- You’re cruising through life, feeling like a budgeting boss, when suddenly—thud.

- Your car breaks down on the highway, your kitchen ceiling starts leaking during a storm, or a “routine” dental visit turns into an expensive root canal.

- In that split second, two options flash in your mind: The Emergency Fund and The Loan.

- Choosing between them isn’t just about math; it’s about timing and strategy.

- Let’s dive into how to navigate this crossroads without losing your cool (or your savings).

We’ve all been there. You’re cruising through life, feeling like a budgeting boss, when suddenly—thud. Your car breaks down on the highway, your kitchen ceiling starts leaking during a storm, or a “routine” dental visit turns into an expensive root canal. In that split second, two options flash in your mind: The Emergency Fund and The Loan.

Choosing between them isn’t just about math; it’s about timing and strategy. Let’s dive into how to navigate this crossroads without losing your cool (or your savings).

The “Safety Net” Logic: Why Cash is King

An emergency fund is your “sleep-at-night” money. It is cash you’ve set aside specifically for life’s surprises. The best part? It’s interest-free. While a loan is essentially renting someone else’s money, your emergency fund is your own cash working for your peace of mind.

But here is a secret: Not every “urgent” event is an “emergency.” A big sale on a new TV? Not an emergency. A broken furnace in the middle of an Illinois winter? Definitely an emergency. Before you dip into that savings bucket, ask yourself: Is it unexpected, necessary, and urgent? If it doesn’t check all three, leave the money where it is and keep your safety net strong.

The Loan Trap: When Borrowing Feels Too Easy

In a world of “Buy Now, Pay Later” and instant app approvals, borrowing money has become very easy. Loans can be a total lifesaver, but they come with a “hangover” called interest. If your budget is already tight, adding a new monthly payment can feel like a heavy weight on your shoulders.

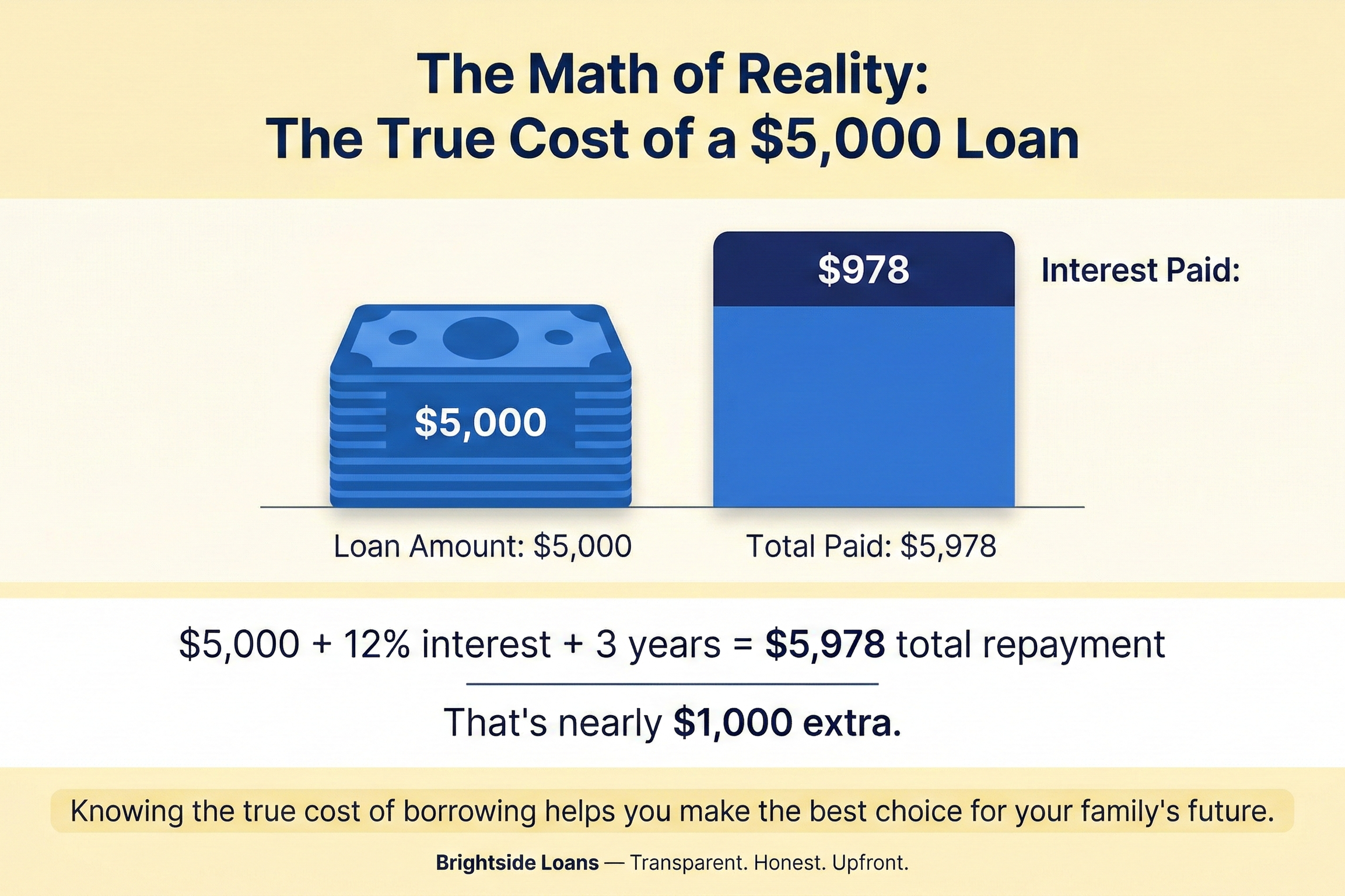

The Math of Reality: If you take out a $5,000 personal loan at a 12% interest rate over three years, you aren’t just paying back $5,000. You’re paying roughly $5,978. That’s nearly $1,000 extra just for the “privilege” of using that money today. This is why having a plan matters. At Brightside Loans, we believe in being upfront—knowing the true cost of borrowing helps you make the best choice for your family’s future.

The “Hybrid” Strategy: A New Perspective

Most experts tell you it’s one or the other. We disagree. Sometimes, the smartest move is to use a Hybrid Approach.

Imagine you have $5,000 in your emergency fund and an unexpected $4,000 repair bill. If you use all your cash, you’re left with almost nothing for the next disaster. Instead, it might be smarter to use $2,000 from your savings and take out one of our affordable personal loans for the other $2,000. This keeps some cash in your pocket while making the loan payment small and easy to manage.

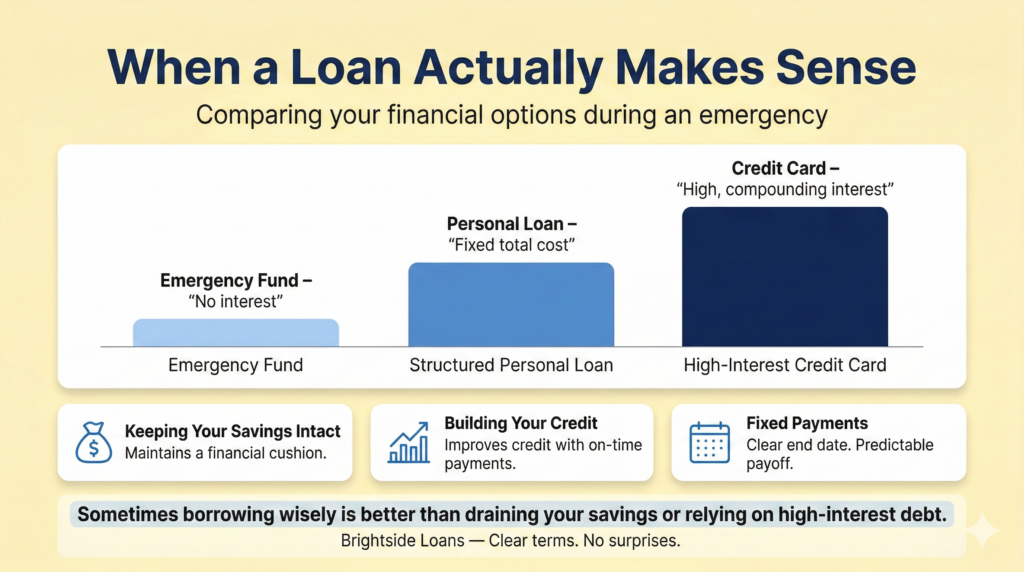

When a Loan Actually Makes Sense

Can a loan ever be the better choice? Sometimes, yes!

- Keeping Your Savings Intact: If using your cash leaves you with $0, a small loan can provide a cushion so you aren’t completely broke if something else goes wrong.

- Building Your Credit: If you are trying to improve your credit score, taking a small loan and paying it back on time is a great way to show banks you are a responsible borrower.

- Fixed Payments: Unlike a credit card where the interest can jump around, a personal loan has a fixed end date. You know exactly when you’ll be debt-free.

Loan Inquiry Form

The Psychological Price Tag

Money is emotional. For some people, debt feels like a heavy chain. For others, seeing an empty savings account causes major stress.

Pro Tip: Figure out your “Stress Floor.” This is the minimum amount of cash you need in the bank to feel safe. Try not to let your savings drop below this number unless it is a true life-or-death emergency.

Comparison at a Glance

| Feature | Emergency Fund | Personal Loan |

| Cost | Free (Zero Interest) | Interest + Fees |

| Approval | Instant (It’s yours!) | Fast Application |

| Risk | Using up your safety net | Monthly payment |

| Impact | Peace of mind | Can help build credit |

The Verdict: Build Your Own Bank

The goal isn’t just to survive a bad day; it’s to bounce back without ruining your budget. Start by building a “Mini-Fund” of $1,000. This handles most of life’s small hiccups, like a flat tire or a broken microwave. Once you have that, try to save up enough to cover three months of bills.

If life throws you a curveball before your savings are ready, Brightside Loans is here to help you bridge the gap with clear terms and friendly Illinois-based support. Apply today to see how we can help you get back on your feet. By the time you reach your savings goal, you won’t just be saving money, you’ll be your own bank.